Stablecoin Cards: A Guide for International Businesses

A stablecoin card is a payment card that enables a business to use stablecoin-backed funds for everyday card transactions through established card payment networks. For international businesses, the value is practical: teams can maintain balances in stablecoins, issue virtual or corporate cards, pay online merchants, apply spending limits, and reconcile global expenses without relying on slow bank-transfer processes for every payment.

However, the card itself is only one component of a complete operating framework. A business-ready program also requires treasury governance, KYC and AML controls, cardholder permissions, merchant restrictions, reporting, and clear rules for when stablecoins are converted or settled. The key question is therefore not only whether a card can be used, but whether the card program is suitable for the company’s operating model.

What is a stablecoin card?

A stablecoin card is a debit, prepaid, corporate, or virtual card product connected to a balance that is funded by, or settled with, stablecoins such as USDC or USDT. The cardholder pays a merchant using standard card credentials, while the provider manages the operational link between the stablecoin balance and the card transaction.

Most business stablecoin cards are virtual-first because international teams commonly need card numbers for software, advertising, travel, vendors, and online subscriptions rather than physical plastic cards. Where mobile-wallet support is available, the card may also be used in person through Apple Pay, Google Pay, or another supported wallet. If you need the broader payment-card foundation first, start with virtual card basics.

A stablecoin card is not the same as a Bitcoin card. Stablecoins are designed to track a reference value, typically a fiat currency such as the U.S. dollar. Bitcoin is more volatile and is not supported by Infini. For business spending, stablecoin cards are useful because they connect a comparatively stable digital treasury asset to everyday card acceptance.

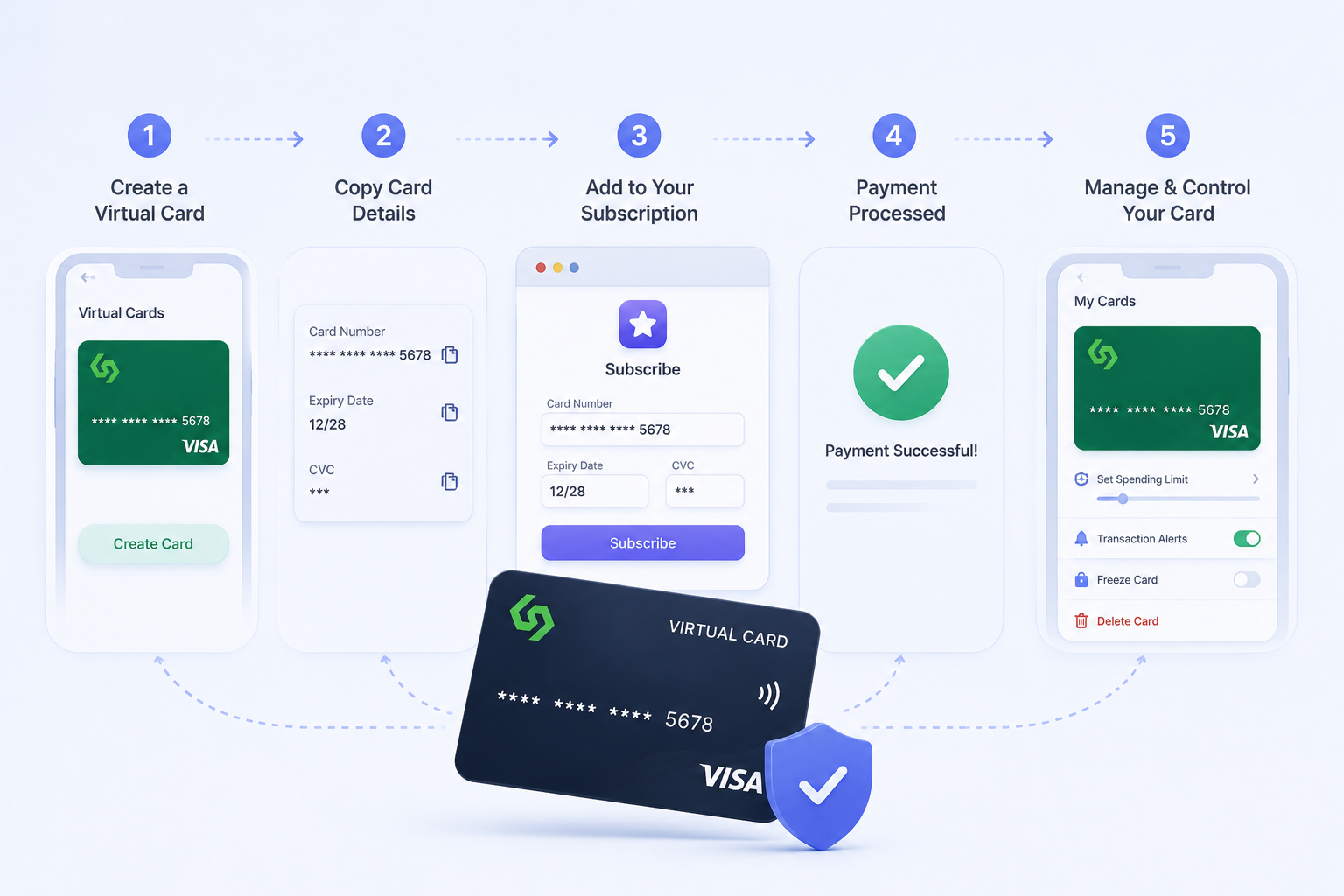

How do stablecoin cards work for international businesses?

Stablecoin cards generally operate across three connected layers: a business funding balance, a card issuing program, and merchant card acceptance. The business funds the account, the provider issues card credentials, and each transaction is authorized according to the provider’s rules. Depending on the provider’s model, stablecoins may be converted before authorization, at settlement, or within the provider’s treasury workflow.

The business funds the account.

The company deposits stablecoins, fiat, or both into the platform, depending on the funding rails supported by the provider.

Finance creates cards.

The team issues a virtual card for an employee, vendor, subscription, campaign, department, or travel budget.

The card is used at checkout.

The merchant receives a standard card payment rather than an onchain transfer.

The provider authorizes the transaction.

The provider reviews card status, limits, merchant rules, balance, country, and authentication requirements.

Funds are converted or settled.

Stablecoin-backed value is applied to the card transaction according to the provider’s settlement model.

Finance reconciles the payment.

The transaction record should include merchant, amount, owner, purpose, currency, status, and supporting metadata.

This is why the mechanics of how virtual cards work remain important. Stablecoin funding changes the treasury layer, but the card still depends on issuer rules, card-network authorization, merchant acceptance, fraud controls, and reconciliation.

For international businesses, the main benefit is operational efficiency. Instead of waiting for local bank accounts, bank wires, or manual reimbursement procedures in each market, finance teams can issue controlled cards close to the moment business spending is required.

How are stablecoin cards different from traditional corporate cards?

The primary difference is the funding and treasury model. A traditional corporate card is typically supported by a bank account, charge account, credit line, or prepaid fiat balance. A stablecoin card connects card spending to stablecoin-based balances or settlement rails, which can be a better fit for companies that already receive, hold, or move stablecoins across borders.

Area | Traditional corporate card | Stablecoin card |

Funding source | Bank account, credit line, debit balance, or prepaid fiat account. | Stablecoin-backed balance, fiat balance, or a dual-track setup depending on the provider. |

Global access | Often depends on local banking relationships and the regional coverage of card issuers. | Can support global teams and stablecoin treasury flows, subject to provider coverage and compliance requirements. |

Settlement | Usually completed through banking systems and card-network settlement in fiat. | The provider may convert or settle stablecoin-backed value into card-network payment obligations. |

Controls | Limits, cardholder permissions, merchant rules, and expense policies vary by provider. | Should provide comparable card controls together with treasury and stablecoin-specific records. |

Accounting | Primarily relies on fiat ledger records and card-statement reconciliation. | Requires clear records for card spend, stablecoin movement, conversion, fees, and fiat-equivalent values. |

Best fit | Companies with conventional banking relationships, credit needs, and local card programs. | International, crypto-native, remote, SaaS, e-commerce, and digital businesses that already operate with stablecoins. |

The funding model is important. Depending on the provider, a stablecoin card may operate more like a prepaid or debit product than a credit product. If your finance team is comparing available balance, authorization holds, and refund handling, it can help to review how prepaid and debit virtual cards differ.

When do stablecoin cards make sense for a business?

Stablecoin cards are most useful when a company operates internationally and needs card-level spending control without adding unnecessary banking friction. The strongest use cases are not broad claims about “crypto payments.” They are specific workflows where distributed teams require fast, controlled access to online spending.

Cross-border e-commerce.

Teams can issue cards for marketplace tools, logistics software, test purchases, subscriptions, and regional operating expenses.

SaaS and online subscriptions.

Finance can assign a dedicated card to each vendor so renewals, upgrades, and cancellations are easier to track. This is especially useful when teams need to

pay subscriptions with a virtual card

.

Digital advertising.

Teams can separate cards by platform, campaign, market, or budget owner instead of sharing one permanent company card.

Remote teams and contractors.

A company can issue controlled cards without shipping physical cards or opening local bank accounts for every team member.

Digital entertainment and creator operations.

Teams that manage multiple platforms, tools, vendors, and regions can isolate payment credentials by use case.

Crypto-native treasury operations.

Businesses that receive revenue or manage liquidity in stablecoins can keep spending closer to their treasury structure.

The fit is weaker when a business mainly uses cash, checks, local offline vendors, or credit-line financing. Stablecoin cards are also not a substitute for tax, compliance, accounting, or treasury policy. They are spending instruments and work best when the surrounding finance process is clearly defined.

What risks and controls should finance teams check?

Finance teams should evaluate stablecoin cards as payment infrastructure, not merely as a convenient application. A card number may be easy to create, but the real risk sits in funding authority, employee access, compliance, merchant acceptance, and reconciliation.

Risk or control | What to check | Why it matters |

KYC and AML | Does the provider conduct business verification and transaction monitoring? | International card programs require a clear compliance foundation. |

Jurisdiction coverage | Which countries, users, and merchant regions are supported or restricted? | A card that works for headquarters may not meet the needs of global teams. |

Stablecoin support | Which stablecoins are supported, and how are conversions handled? | Unsupported assets or unclear conversion timing can create treasury and accounting issues. |

Spend limits | Can finance set per-card, per-user, vendor, daily, monthly, or campaign limits? | Limits prevent a single credential from becoming an uncontrolled source of company spending. |

Merchant controls | Can the provider restrict merchant categories, vendors, countries, or use cases? | Policy must be enforceable at the payment level. |

Freeze and termination | Can cards be paused or closed immediately? | Vendor changes, employee departures, and suspected fraud require rapid response. |

Records and reporting | Does each transaction show owner, purpose, merchant, currency, fee, and status? | Stablecoin-funded spending still needs to reconcile cleanly. |

Regulation is also changing quickly. Companies should review stablecoin regulation for businesses before treating a card rollout as a procurement-only decision. The right provider should make compliance information visible rather than leaving finance teams to resolve uncertainty after launch.

What should businesses look for in a stablecoin card provider?

Businesses should choose a provider that supports the full operating workflow: funding, card issuance, spending controls, reporting, compliance, customer support, and treasury visibility. A simple signup process is helpful, but it is not sufficient for finance teams that require repeatable control.

Business-grade onboarding.

The provider should support company verification, authorized users, and clear eligibility rules.

Virtual card issuance.

Finance should be able to create cards by person, vendor, project, subscription, campaign, or team.

Real-time controls.

Limits, card status, merchant rules, and budget controls should be easy to adjust.

Stablecoin and fiat rails.

The product should match how the company actually receives, holds, and spends funds.

Transparent fees.

Card fees, conversion costs, account fees, and hidden charges should be visible before rollout.

Reporting and reconciliation.

Finance needs structured transaction records, not only card numbers.

Support and issue handling.

Declines, refunds, disputes, and cardholder questions need a clear operating process.

Program fit.

The card should support the company’s broader

, not create a separate shadow process.

If your team is comparing stablecoin cards with more conventional providers, use a broader framework to choose the right corporate card solution. The best provider gives finance sufficient control while allowing legitimate business spending to proceed efficiently.

How does Infini's corporate card fit stablecoin business spending?

Infini’s corporate cards are designed for international businesses that need card issuance, stablecoin settlement rails, and spending controls within one financial operating system. The product addresses a common challenge for global teams: funds may move across borders efficiently, while everyday business spending still relies on fragmented cards, shared credentials, manual approvals, and difficult reconciliation.

Infini is an AI-powered financial OS for global business. The platform brings together stablecoin payments, corporate virtual cards, treasury management, and financial automation so teams can manage spending in a way that better reflects modern internet business operations. It is especially relevant for cross-border e-commerce, SaaS, and digital entertainment companies that need to pay online merchants, tools, vendors, and distributed teams across markets.

For card operations, Infini focuses on practical controls: virtual card issuance, dedicated card budgets, real-time spending visibility, and the ability to freeze or terminate cards when a vendor, employee, project, or campaign changes. Stablecoin settlement rails help connect card spending to modern treasury operations instead of forcing every workflow back into slower banking channels.

The pricing model is intentionally straightforward: a flat 0.3% fee, with no monthly fee, no account opening fee, and no hidden fees. Infini supports a fiat and stablecoin dual-track model, is KYC and AML enabled, and supports most countries and regions worldwide excluding Mainland China and sanctioned jurisdictions.

The practical benefit is not simply the ability to create another card. It is the ability to create a controlled payment object for a defined purpose, connect it to treasury operations, monitor spending in real time, and close access when that purpose ends.

How should a company roll out stablecoin cards safely?

A safe rollout should begin with a limited scope, a clearly defined use case, and measurable controls. Companies should not start by replacing every corporate card workflow. Instead, they should begin where stablecoin-funded card spending removes a real operational bottleneck and where finance can monitor the results.

Choose the first use case.

Start with a controlled category such as SaaS subscriptions, ad accounts, contractor tools, or one international team.

Define the policy.

Document who can request cards, which stablecoins or funding rails are permitted, which merchants are approved, and how exceptions are handled.

Assign ownership.

Every card should have a named owner, purpose, budget, and review cadence.

Set limits before issuing cards.

Use transaction, daily, monthly, vendor, and campaign limits where available.

Test important merchants.

Run small payments before relying on a new card for critical spending.

Plan wallet use separately.

If employees need in-person payments, confirm whether they can

add a virtual card to Apple Pay or Google Pay

.

Reconcile early.

Confirm that finance can match card spend, stablecoin movement, fees, owners, and approvals.

Scale by workflow.

Add teams, vendors, or regions only after the first category operates reliably.

This approach keeps the rollout controlled and practical. A stablecoin card program should increase financial visibility and control, not create another payment channel operating outside company policy.

FAQ

Are stablecoin cards legal for businesses?

They can be legal, but this depends on the provider, jurisdictions, customer type, supported assets, and compliance model. Businesses should select providers with clear KYC, AML, licensing, and regional eligibility rules, and should review local legal and tax obligations before launch.

Do merchants need to accept stablecoins?

No. In a typical stablecoin card setup, the merchant receives a standard card payment through card acceptance rails. The stablecoin component operates behind the card program and treasury workflow.

Can a stablecoin card replace a corporate credit card?

In some cases, yes, but not in every case. A stablecoin card may replace prepaid or debit-like spending workflows, especially for online global expenses. It may not replace a credit product when the company depends on credit terms, rewards, or local banking features.

Do stablecoin cards support physical cards?

Some providers support physical cards, but many business use cases remain virtual-first. For international teams, virtual cards are often more useful because they can be issued quickly for vendors, subscriptions, campaigns, and employees.

What fees should businesses expect?

Businesses should review card transaction fees, account fees, conversion fees, withdrawal fees, foreign exchange costs, and hidden minimums. Infini’s corporate card pricing uses a flat 0.3% fee with no monthly fee, no account opening fee, and no hidden fees.

What is the biggest mistake when adopting stablecoin cards?

The biggest mistake is treating stablecoin cards as isolated card numbers rather than as part of a finance workflow. A safer approach is to connect each card to an owner, purpose, budget, funding policy, approval process, and reconciliation record.