How Do Virtual Cards Work?

Virtual cards operate by issuing a set of digital card credentials and linking those credentials to a designated funding source, such as a credit line, debit account, prepaid balance, wallet balance, or corporate card account. When a user pays online or through a supported mobile wallet, the merchant submits the card details through the standard card network. The issuer or card provider then evaluates the transaction against available funds, spending limits, merchant rules, and security requirements before approving or declining the payment.

The essential point is that a virtual card is generally not a separate payment network. It usually relies on the same card rails and issuing rules as a physical card. The difference is that the credential is digital, which makes it easier to issue, configure, pause, replace, and close.

What is a virtual card?

A virtual card is a payment card that exists as digital credentials rather than as a physical piece of plastic or metal. It typically includes a card number, expiration date, and security code, and it can be used wherever the merchant accepts the relevant card type and the provider permits the transaction.

Virtual cards may be connected to different funding models. Some are virtual credit cards, some are linked to debit accounts, some are prepaid cards, and others are corporate cards issued within a business spend platform. If you need the broader concept before reviewing the mechanics, start with the guide to virtual card basics.

The digital format gives providers and users more control over the card lifecycle. A virtual card can often be created instantly, assigned to a specific merchant or employee, limited to a budget, locked after use, or deleted without replacing a physical card.

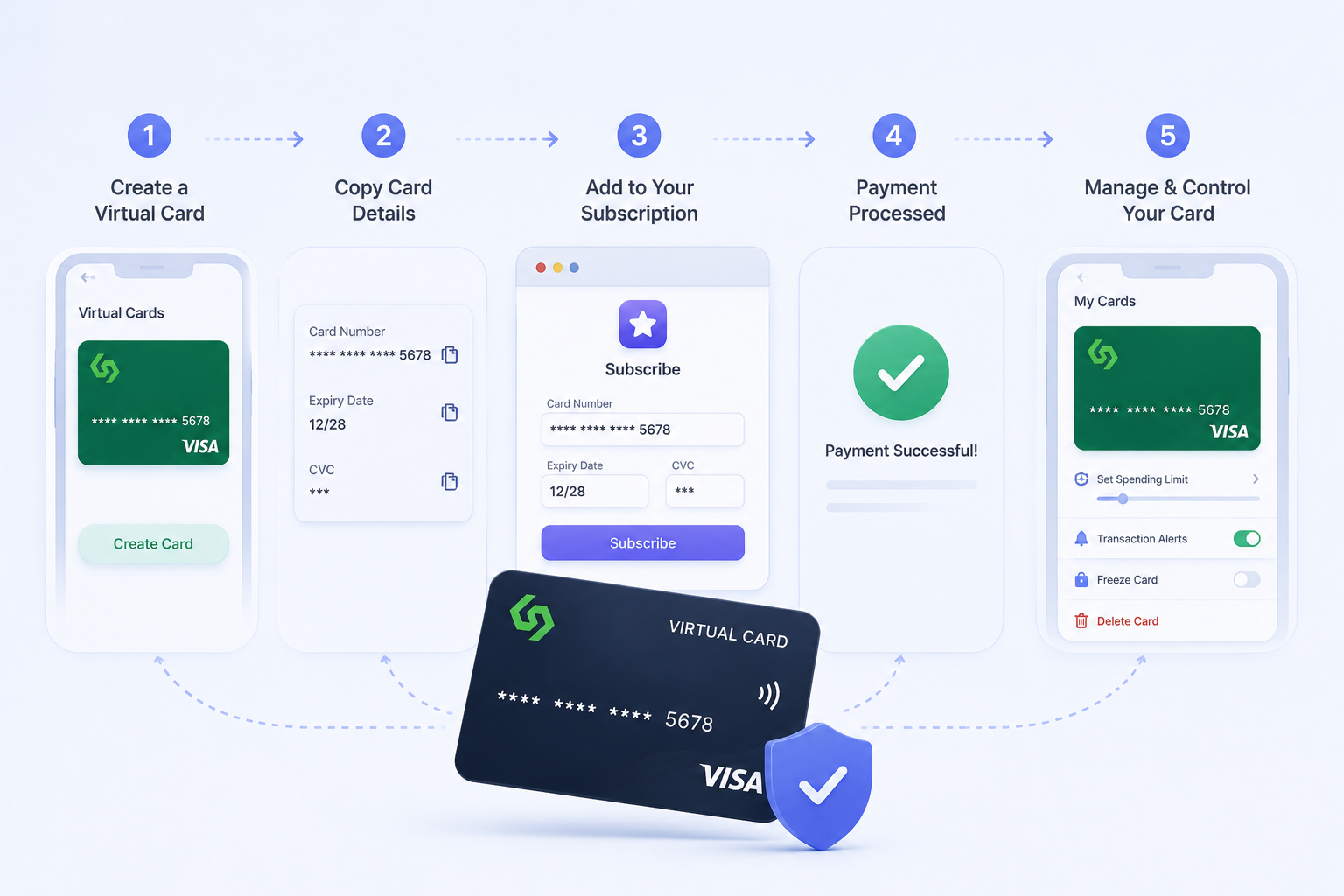

How do virtual cards work step by step?

A virtual card follows a structured process: the provider creates the card credentials, connects them to a funding source, applies usage rules, and processes payments through the card network when the card is used.

The user or business creates a card.

This may take place in a banking app, card issuer dashboard, wallet, browser extension, or corporate spend platform.

The provider assigns card credentials.

The card receives a number, expiration date, and security code. It may be configured as single-use, reusable, merchant-specific, or assigned to a specific team member.

The card is linked to a funding source.

Depending on the program, the funding source may be a credit account, bank balance, prepaid balance, stablecoin balance, or corporate card account.

Rules are applied.

The provider can enforce transaction limits, merchant categories, country restrictions, expiration dates, wallet permissions, and approval workflows.

The card is used at checkout.

The user enters the virtual card details online or pays through a mobile wallet if wallet provisioning is supported.

The transaction is authorized or declined.

The merchant, network, issuer, and provider verify whether the transaction complies with the applicable card and account rules.

The payment settles and records are created.

After authorization, the transaction clears, funds move according to the card program, and records are generated for statements, accounting, or reconciliation.

For users preparing to set one up, the practical next step is usually to learn how to get a virtual credit card or virtual business card from a provider that supports the intended use case.

What happens when you pay with a virtual card?

When a virtual card is used online, the checkout experience appears familiar, but several verification steps occur in the background. The merchant collects the card number, expiration date, CVV, billing address, and, in some cases, a 3D Secure or app-confirmation step. The merchant's payment processor then sends an authorization request through the card network to the issuer or provider.

The issuer or provider evaluates the transaction. It checks whether the card is active, whether the amount is within the permitted limit, whether the merchant is allowed, whether the billing information matches, whether additional authentication is required, and whether the funding source can cover the payment. If the checks pass, the merchant receives an approval. If any requirement is not met, the card may be declined.

An authorization is not always the final charge. Hotels, car rentals, fuel stations, and some online merchants may place an initial hold and finalize the amount later. Refunds usually return through the original card route, even when the card is virtual, although timing depends on the merchant, network, and provider.

Recurring payments require particular attention. A one-time virtual card may fail on the next billing cycle, while a reusable card can continue supporting a subscription. For software, advertising platforms, and other renewals, use a card designed to pay subscriptions with a virtual card.

How are virtual cards different from physical cards?

Virtual and physical cards often operate on the same payment network logic. The key differences are the card format, the control model, and lifecycle management.

Dimension | Virtual card | Physical card |

Format | Digital card credentials displayed in an app or dashboard. | Plastic or metal card with a chip, magnetic stripe, and printed details. |

Issuance | Often created instantly and assigned to a defined purpose. | Usually requires production, shipping, and physical handoff. |

Controls | Can often include per-card limits, merchant rules, expiration rules, and freeze controls. | Controls depend on the issuer and program, but replacing the card is typically slower. |

Security | Can isolate the main account number and reduce exposure to individual merchants. | The same card number is often reused across many merchants until it is replaced. |

In-store use | Usually requires Apple Pay, Google Pay, or another supported wallet. | Works wherever the card type and physical terminal are accepted. |

Lifecycle | Can be created, paused, deleted, or replaced quickly. | Replacement usually involves canceling and reissuing a physical card. |

Funding type is separate from card format. A virtual card can be prepaid, debit-linked, credit-linked, or corporate. If the funding model affects your use case, compare prepaid and debit virtual cards before relying on the card for an important payment.

Are virtual cards safer than regular cards?

Virtual cards can provide stronger security controls because they reduce how often a primary card number or account credential is shared. A provider may allow a user or business to create a dedicated card for one merchant, one purchase, one subscription, one employee, or one budget. If that card credential is exposed, it can be locked or closed without disrupting every other payment relationship.

Some virtual card and mobile wallet flows also use tokenization. Tokenization replaces sensitive card data with a substitute value that can be limited to a specific device, merchant, or transaction context. This can reduce the usefulness of stolen payment data because the token is not the same as the underlying account credential.

Virtual cards are not a complete security solution on their own. They do not automatically prevent phishing, weak passwords, account takeover, social engineering, or poorly designed approval processes. They are most effective when combined with account security, clear spending rules, trusted devices, strong authentication, and regular review of active cards.

Where can you use a virtual card?

A virtual card can usually be used for online checkout wherever the merchant accepts the relevant card network and the provider allows the transaction. Common uses include ecommerce purchases, software subscriptions, advertising accounts, travel bookings, supplier invoices, app purchases, and card-on-file payments.

In-store use depends on wallet support. If the virtual card can be added to Apple Pay, Google Pay, or another accepted wallet, the user may be able to tap a phone at a contactless terminal. If the merchant requires a chip card, swipe card, cash withdrawal, or a physical card at check-in, a virtual card may not be sufficient.

Card network and issuer rules remain important. A guide on how to use a virtual Visa card can be helpful when the virtual card is issued on Visa rails, while a wallet-specific guide can help you add a virtual card to Apple Pay or Google Pay for supported in-person payments.

Why do virtual card payments fail?

A virtual card payment usually fails because the card details, merchant context, provider rules, or funding source do not match the attempted transaction. The card may be valid, but the specific payment may still violate a limit or checkout requirement.

Failure reason | What it means | What to check |

Wrong card details | The number, CVV, or expiration date was entered incorrectly. | Copy the latest details directly from the provider. |

Billing address mismatch | The merchant's address check does not match issuer records. | Use the billing address required by the provider. |

Limit exceeded | The amount is above the card's transaction, daily, monthly, or total limit. | Increase the limit or choose a card with sufficient available budget. |

Merchant blocked | The card program blocks the merchant, category, country, or risk type. | Review merchant category and country rules. |

Single-use card reused | The card was configured for one transaction and cannot be charged again. | Create a reusable card for renewals and subscriptions. |

Wallet unsupported | The card works online but cannot be provisioned into a mobile wallet. | Confirm Apple Pay or Google Pay support before relying on in-store use. |

Authentication failed | 3D Secure, app approval, or one-time password verification was not completed. | Retry after completing the issuer's verification step. |

Card frozen or expired | The card was paused, deleted, expired, or closed by policy. | Unfreeze the card if allowed or issue a new one. |

For businesses, decline troubleshooting is easier when every card has a clear owner, purpose, budget, merchant rule, and expiry policy. Without that context, finance teams may spend unnecessary time determining whether the issue is related to the merchant, the funding source, or an intentional policy block.

How do businesses use virtual cards for spend control?

Businesses use virtual cards to turn payment access into a configurable and auditable object. Instead of sharing a single company card across employees, vendors, and subscriptions, a team can issue dedicated cards for specific purposes and close them when those purposes end.

Business use case | How the virtual card works | Control to apply |

Software subscriptions | One reusable card for one SaaS vendor. | Monthly limit, owner, renewal review date. |

Ad spend | One card per campaign, platform, or market. | Campaign budget, merchant rule, daily cap. |

Contractors or remote teams | Cards issued without shipping physical plastic. | Role-based limit, country rules, expiry date. |

Travel booking | Trip-specific cards for flights, hotels, and booking platforms. | Trip budget, merchant category rules, end date. |

Supplier payments | Vendor-specific cards for online invoices or portals. | Vendor lock, approval workflow, reconciliation note. |

This is why virtual cards often sit inside broader corporate card programs. The card number is only one component of the system. The broader value is visibility: who owns the payment, why it exists, what limit applies, which merchant can charge it, and when it should be terminated.

When companies evaluate providers, they should look beyond card creation speed. They should assess how the product handles budgets, approvals, merchant restrictions, accounting exports, support, currencies, wallet use, refunds, and card lifecycle management. That evaluation belongs within the broader process of choosing the right corporate card solution.

How does Infini support virtual card workflows for global teams?

Infini supports virtual card workflows through corporate cards built for global business spend. The product is designed for teams that need card issuance, dedicated card controls, real-time budgets, spend visibility, and the ability to freeze or terminate cards when an employee, vendor, campaign, or subscription changes.

Across cross-border ecommerce, SaaS, and digital entertainment companies, we see a consistent operational pattern: the payment challenge is rarely limited to obtaining a card number. The more important requirement is connecting that card number to treasury, policy, ownership, and reconciliation across markets.

Infini is an AI-powered financial OS for global businesses, combining corporate virtual cards with fiat and stablecoin workflows. Its corporate cards are built for teams that want virtual cards inside a broader financial operating system rather than isolated payment credentials. Infini's corporate card pricing is structured as a flat 0.3% fee, with no monthly fee, no account opening fee, and no hidden fees.

For finance teams, this means a virtual card can become part of a controlled spend workflow: issue the card for a defined purpose, set a budget, monitor activity, reconcile the transaction, and close the credential when the business relationship ends.

FAQ

Is a virtual card a real card?

Yes. A virtual card is a real payment credential. It can be authorized through card networks like a physical card, but the credential exists in digital form rather than on plastic.

Is a virtual card linked to my real card or bank account?

Usually yes, but the exact link depends on the provider. A virtual card may be linked to a credit account, debit account, prepaid balance, business wallet, stablecoin balance, or corporate card account.

Can I use a virtual card more than once?

It depends on the card type. Some virtual cards are single-use, while others are reusable for one merchant, one subscription, one employee, or general online spending.

Can a virtual card replace a physical card?

A virtual card can replace a physical card for many online and wallet-supported payments. It may not replace a physical card for ATMs, offline merchants, or locations that require a chip or swipe card.

What happens if I need a refund on a virtual card?

The refund usually returns through the original card route and is credited back to the underlying account or balance. Timing depends on the merchant, card network, and provider.

Do virtual cards help businesses control spending?

Yes. Businesses can use virtual cards to assign payment access by employee, vendor, subscription, project, campaign, or travel booking, and then apply limits, rules, ownership, and expiry dates to each card.