Once upon a time, the stablecoin market resembled the "Wild West," growing unchecked with little regulation. But this scenario is undergoing a seismic shift: the U.S. Congress has introduced the Stablecoin Transparency and Accountability for a Better Ledger Economy Act of 2025 (referred to as the *STABLE Act*). This legislation aims to impose strict regulations on stablecoins—requiring issuers to obtain licenses, maintain full reserves, refrain from paying interest, and disclose information regularly. A regulatory storm is brewing around stablecoins. How will it reshape this multi-billion-dollar market?

Overview of the Act’s Key Provisions

The STABLE Act, proposed by bipartisan members of the U.S. House of Representatives in 2025, seeks to establish a clear regulatory framework for dollar-denominated payment stablecoins. Its main requirements can be summarized as follows:

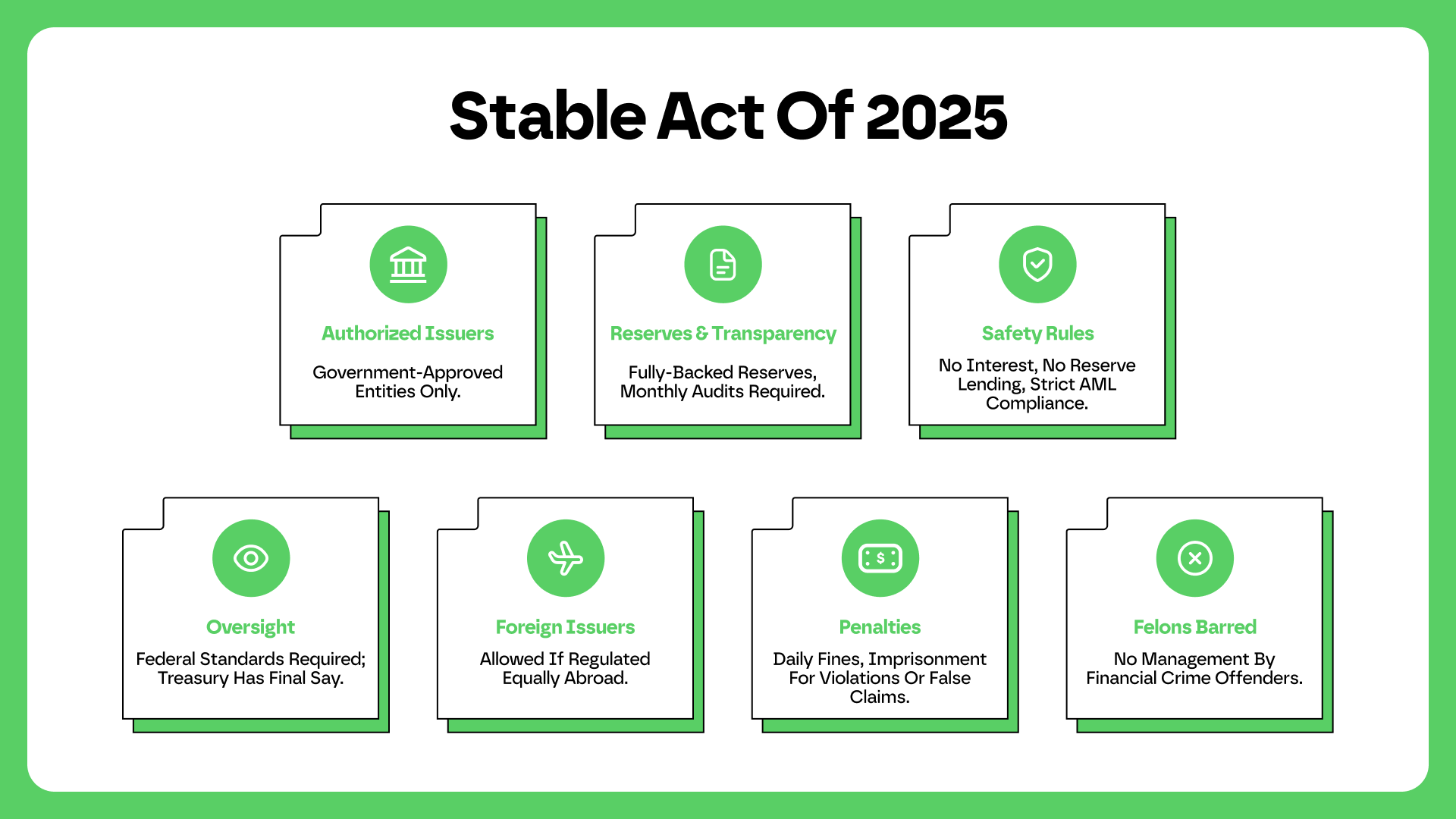

Licensing Requirements: Stablecoin issuers must obtain regulatory approval to become "qualified issuing institutions." The Act categorizes qualified issuers into three types: federally regulated depository institutions (e.g., banks, credit unions), non-bank entities approved by the Office of the Comptroller of the Currency (OCC), and state-licensed institutions operating under a federally certified system. In other words, whether a bank or a non-bank company, all must either hold a federal license or operate under state supervision that meets federal standards. Unauthorized issuers face severe penalties, including fines of up to $100,000 per day.

1:1 Reserve Backing: Issued stablecoins must be fully backed (100%) by high-quality liquid assets of equivalent value. Eligible reserve assets include cash, demand deposits in regulated banks, short-term U.S. Treasury bonds, central bank reserves, and other safe assets. This ensures each stablecoin is adequately collateralized, preventing "reserve shortfalls" that could trigger runs.

Prohibition on Interest/Yield Payments: The Act explicitly bans stablecoin issuers from paying interest or other yields to holders. Stablecoin accounts thus cannot earn interest like bank deposits. This rule aims to prevent stablecoins from becoming unapproved deposit products that disrupt financial order. It also distinguishes stablecoins from yield-bearing securities, avoiding securities law implications.

Disclosure and Auditing: Issuers must regularly disclose reserve status and redemption policies to the public and undergo independent audits. Specifically, the Act requires issuers to provide monthly reserve attestations, verified by certified public accounting firms and signed by the CEO and CFO to certify accuracy. Regulators must also report annually on licensing progress. Executives who knowingly provide false attestations may face criminal liability, including fines of up to $1 million or 10 years in prison. These stringent disclosure rules aim to enhance transparency, allowing the public and regulators to monitor stablecoin safety in real time.

Business Scope Restrictions: To mitigate risks, the Act strictly limits issuers to core functions, such as issuing and redeeming stablecoins and providing related custodial services. Issuers cannot engage in traditional banking activities like lending, and reserve assets cannot be pledged or reinvested (except for redemption liquidity needs under strict conditions). By enforcing "activity separation," the Act ensures issuers focus on stablecoins without diverting user funds to high-risk ventures.

In summary, the STABLE Act establishes fundamental rules for the stablecoin industry: licensed operation, full collateralization, transparent operations, and a focus on core functions. This marks a shift from a relatively unregulated environment to a compliance era akin to regulated financial institutions.

Non-Banks, Bank Subsidiaries, and State Oversight: Who Regulates Stablecoins?

The STABLE Act pays special attention to regulatory arrangements for different types of issuers, seeking a balance between federal and state oversight. Under the Act, issuers have three primary pathways, each with distinct regulatory implications:

Federally Chartered Non-Bank Issuers: For tech/crypto companies like Circle (issuer of USDC) that are not banks, the Act provides a federal licensing route—approval by the OCC as a federally recognized stablecoin issuer. These licensed entities will be primarily supervised by the OCC and must comply with federal capital, liquidity, and risk management requirements while facing coordinated oversight from agencies like the Federal Reserve and FDIC. The federal license offers nationwide applicability but involves rigorous scrutiny.

Banks and Their Subsidiaries: Commercial banks may issue stablecoins, typically through subsidiaries to isolate risks. For bank-affiliated issuers, the Act follows the principle of "existing regulators remain in charge." For example, if JPMorgan issues stablecoins via a subsidiary, its primary federal regulator (e.g., the Fed or OCC) would oversee the activity. Banks must still adhere to 1:1 reserve rules but benefit from existing regulatory frameworks. This levels the playing field between banks and tech firms while subjecting banks to their own prudential standards.

State-Regulated Issuers: Some states (e.g., New York, Wyoming) already have digital asset licensing regimes (e.g., New York’s trust charter). The Act acknowledges state roles: if an issuer holds a state license and the state framework is deemed "substantially equivalent" to federal standards, the issuer may operate under state oversight. This grants federal recognition to state-compliant stablecoins (e.g., Paxos-issued PayPal USD in New York), allowing nationwide circulation. However, to prevent regulatory arbitrage, the Act establishes a certification mechanism—federal agencies will assess whether state rules meet federal benchmarks, with non-compliant states potentially requiring issuers to switch to federal oversight.

Notably, earlier debates over stablecoin regulation revolved around "federal vs. state" authority. Some advocated for exclusive federal oversight (fearing inconsistent state standards), while others argued for recognizing qualified state regimes to avoid stifling innovation. The STABLE Act strikes a compromise—offering federal licensing while accommodating state frameworks if equally robust. Issuers can choose the most suitable path, minimizing disruption for existing state-licensed players (e.g., Paxos, Circle) while gradually unifying industry standards.

Potential Shifts in the Stablecoin Market Landscape

Once enacted, this landmark legislation will profoundly reshape the stablecoin market, currently valued at over $230 billion and growing for 18 consecutive months. Among the dominant players, Tether (USDT) and USD Coin (USDC) face divergent futures under the *STABLE Act*:

Tether (USDT): As the largest stablecoin by market cap (~$144 billion), USDT has long operated outside U.S. regulation, with its issuer (a non-U.S. entity) facing transparency concerns. If the Act passes, USDT must either comply (disclosing finances, undergoing audits) or exit compliant U.S. channels. Given monthly audit requirements, USDT’s opaque practices may become untenable. Recently, Tether hinted at launching a U.S.-compliant stablecoin, signaling adaptation. Non-compliance could marginalize USDT in the U.S., while compliance may force operational overhauls—a pivotal crossroads for the industry giant.

USD Coin (USDC): Issued by U.S.-based Circle and Coinbase, USDC has proactively embraced compliance, holding state money transmitter licenses and publishing monthly reserve reports. Aligning closely with the Act, USDC’s issuer will likely seek an OCC federal license, solidifying its U.S. position and gaining institutional trust. With its transparent image, USDC could attract risk-averse capital, potentially expanding its market share. However, higher compliance costs (e.g., executive liability) are inevitable.

PayPal USD (PYUSD): Launched in 2023 by PayPal (issued by NYDFS-licensed Paxos), PYUSD represents stablecoin adoption by mainstream finance. Its state-regulated model (New York) is expected to qualify under federal recognition. Already compliant with full-reserve and disclosure rules, PYUSD may emerge stronger, with regulatory clarity boosting credibility. The Act could encourage more fintech giants to enter the space, intensifying competition.

Other stablecoins (e.g., algorithmic or commodity-backed) fall outside the Act’s immediate scope, pending further study. Decentralized options like DAI remain unaffected for now but may face future rules. Overall, the Act will elevate compliant stablecoins while sidelining "unlicensed" ones. Licensed issuers (federal or state) may gain market confidence and institutional adoption, while non-compliant ones risk losing mainstream access. For the industry, this regulatory overhaul presents both opportunities and challenges: a shakeup is inevitable, but long-term credibility and maturity could position stablecoins as true pillars of the digital economy.

The Act’s Background and Underlying Motivations

The U.S. push for stablecoin legislation stems from both practical pressures and strategic calculations, culminating in a long-gestating effort.

Policy Consensus: Both Democrats and Republicans recognize the urgency of regulation. In 2021, Biden’s Presidential Working Group called for Congressional action to mitigate risks. By 2025, the new administration prioritized digital asset innovation, with the White House endorsing dollar-backed stablecoins to bolster U.S. leadership in digital finance. A Republican president even emphasized "strengthening U.S. fintech dominance," encouraging stablecoin innovation. High-level consensus set the tone: stablecoins must be regulated, with the U.S. leading rulemaking rather than standing idle.

Market Realities: Explosive stablecoin growth (from billions to hundreds of billions) and crises like Terra/Luna’s collapse (2022) and USDC’s temporary depeg (2023) underscored regulatory gaps. Congress realized that without rules, the next crisis could be catastrophic. Protecting consumers and financial stability demanded preemptive action. As Rep. Torres noted, "Stablecoins represent fintech’s next frontier—the U.S. must lead in shaping their framework."

Dollar Hegemony: Stablecoins, as blockchain-based dollar proxies, have become global dollar alternatives. Regulating them effectively extends dollar dominance into digital realms. Drafters openly stated the Act ensures "dollar primacy in future payments." Bringing stablecoins into the fold prevents uncontrolled alternatives from undermining traditional monetary policy. The U.S. also aims to shape global standards, retaining influence in the digital currency race.

Bipartisan Compromise: Earlier partisan divides (Democrats favoring strict federal control, Republicans advocating flexibility) gave way to compromise. The STABLE Act merges both approaches—federal licensing with state recognition—reflecting rare cross-party alignment on crypto. The urgency stemmed from a shared realization: internal gridlock risks ceding innovation to others.

Conclusion: Will Regulation Usher in a More Stable Future?

As an observer, I view the STABLE Act with cautious optimism. On one hand, it promises to end the wild west era, fostering a market where only transparent, fully backed stablecoins thrive. This protects consumers and paves the way for institutional adoption—imagine seamless stablecoin integration in mainstream finance, invisible to end-users. By setting a global precedent, the U.S. could steer international standards, a promising prospect. Yet, excessive regulation risks stifling innovation. Stablecoins flourished partly due to entrepreneurial experimentation in regulatory gray zones. Overly stringent rules may deter startups, entrenching incumbents and dampening dynamism. Offshore issuers like USDT might resist compliance, limiting the Act’s global reach. Implementation hurdles—regulatory coordination, state-federal alignment, technical execution—could also trigger short-term turbulence. Regardless, the STABLE Act marks a turning point, bringing stablecoins into the regulatory sunlight. Like the early internet, blockchain finance must eventually embrace oversight. In the long run, regulation may foster a "Better Ledger Economy"—transparent, trusted, and stable. Whether stablecoins achieve true stability, bridging traditional and crypto finance, hinges on this U.S. move, which may define the sector’s trajectory for years to come.